In a shifting real estate market, the guidance and expertise that Inman imparts are never more valuable. Whether at our events, or with our daily news coverage and how-to journalism, we’re here to help you build your business, adopt the right tools — and make money. Join us in person in Las Vegas at Connect, and utilize your Select subscription for all the information you need to make the right decisions. When the waters get choppy, trust Inman to help you navigate.

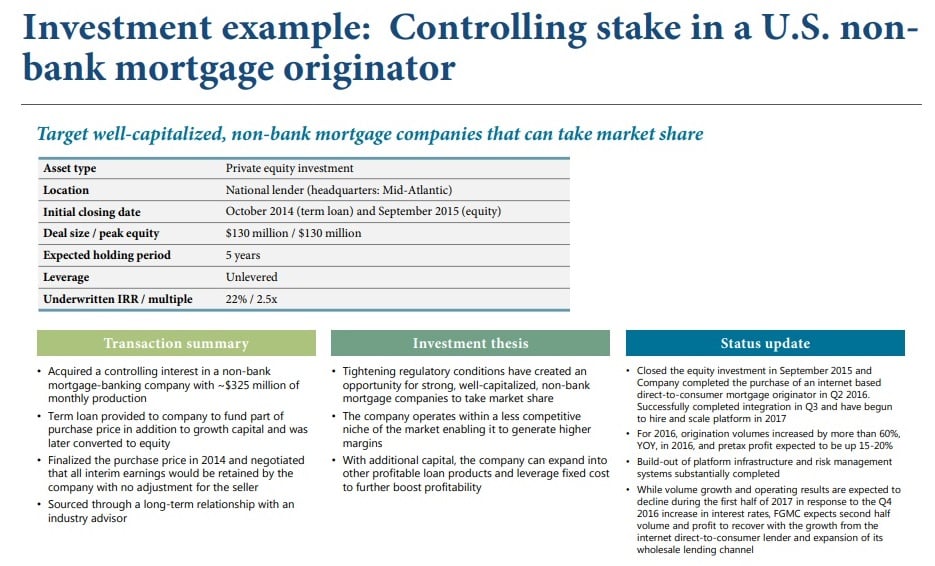

When the investment management firm PIMCO purchased a nonbank lender, First Guaranty Mortgage Corp. in 2015, the company saw an opportunity to “Do what banks can’t or won’t do” in the face of tightening regulations: Provide mortgages to riskier borrowers.

In a 2017 investor presentation seeking billions to pursue similar deals, PIMCO portrayed its acquisition of FGMC as an example of how its broader investment strategy — to make opportunistic investments in markets subject to regulatory reform including mortgage and real estate — could exploit an untapped niche.

PIMCO also revealed it was banking on unloading its investment in FGMC within 5 years; a plan that’s now apparently gone awry. With rising mortgage rates wreaking havoc on the mortgage industry as a whole, FGMC laid off 76 percent of its workforce on June 24 and Thursday filed for Chapter 11 bankruptcy protection from creditors.

In a 2017 investor pitch for its BRAVO Fund III PIMCO detailed how it acquired a controlling interest in FGMC in 2014: By providing a term loan that was later converted to equity.

PIMCO’s pitch to the New Mexico State Investment Council envisioned a bright future for FGMC with the potential to grow the nonbank lender’s $325 million in monthly loan originations by making additional investments in the company, which was based in Maryland at the time.

“Tightening regulatory conditions have created an opportunity for strong, well-capitalized, non-bank mortgage companies to take market share,” PIMCO said of its strategy. FGMC, it said, “operates within a less competitive niche of the market enabling it to generate higher margins. With additional capital, the company can expand into other profitable loan products and leverage fixed [costs] to further boost profitability.”

Excerpt from February 2017 PIMCO investor presentation to New Mexico State Investment Council

After PIMCO closed its $130 million equity investment in FGMC in September 2015, the company acquired an online direct-to-consumer mortgage originator GoodMortgage.com and boosted loan originations by 60 percent in 2016.

“While volume growth and operating results are expected to decline during the first half of 2017 in response to the Q4 2016 increase in interest rates, FGMC expects second-half volume and profit to recover with the growth from the internet direct-to-consumer lender and expansion of its wholesale lending channel,” PIMCO noted in its investor presentation, foreshadowing the company’s more recent difficulties.

Mortgage rates on a roller coaster ride

Mortgage rates would surge again in 2018 only to tohistoric lows during the pandemic, as the Federal Reserve purchased trillions in government debt and mortgage-backed securities in order to keep the economy from crashing by making it cheaper to borrow.

As the Fed wrapped up its “quantitative easing” and started raising short-term rates this year, mortgage rates surged above 6 percent forcing many mortgage lenders to downsize as the lucrative business of refinancing existing homeowners’ mortgages dried up.

Appetite for ‘non-QM’ loans

In addition to rising interest rates, another potential headwind for FGMC is that it specializes in non-QM loans which don’t meet underwriting standards for so-called “qualified mortgages” eligible for purchase by Fannie Mae and Freddie Mac. That can make them more difficult to bundle into mortgage-backed securities that are sold to investors.

In its February 2017 investor presentation to the New Mexico State Investment Council PIMCO said it saw non-QM loans as an opportunity to “take advantage of the spread differential between conforming and non-conforming mortgage rates.”

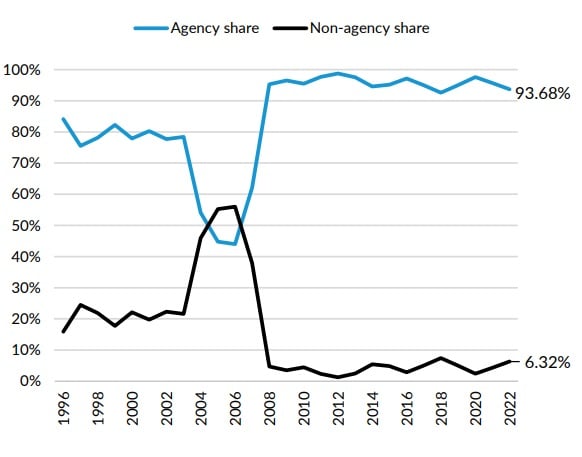

By the end of 2016 PIMCO said it had purchased $750 million in non-QM loans from five different sellers including $517 million in 2016 alone and was moving forward with plans to complete its first non-QM securitization in early 2017 with the aim of reselling those loans at a profit. PIMCO was at the cutting edge of a resurgence in “non-agency” securitizations, which dried up in the wake of the 2007-09 housing crash and recession.

Agency share of mortgage securitizations

Non-agency securitizations plunged in 2007 due to high default rates on subprime mortgage loans. Source: Urban Institute.

The vast majority of mortgages that bundled up into mortgage-backed securities for sale to investors are qualified mortgages that are either purchased or guaranteed by Fannie Mae and Freddie Mac or backed by the FHA, VA and USDA and securitized by Ginnie Mae (“the agencies”). The agency share of mortgage securitizations which dropped below 50 percent as subprime lending fueled the 2004-06 housing bubble has rebounded to above 90 percent, according to the Urban Institute.

The market for non-agency mortgage-backed securities almost dried up during the pandemic, accounting for just 2.44 percent of mortgage securitizations in 2020. But non-agency securitizations bounced back last year, accounting for 4.32 percent of mortgages packaged into securities for sale to investors — the highest share since 2008.

PIMCO raised $12 billion for series of ‘opportunistic’ funds

In its 2017 investor presentation seeking up to $5 billion in investments in its BRAVO Fund III, PIMCO laid out the opportunity to profit by serving borrowers not eligible for qualified mortgages.

With banks “purposefully ceding market share in targeted residential markets” due to stricter capital requirements, punitive fines and regulatory action a “sizable universe of potential borrowers remain unable to access mortgage credit,” PIMCO told prospective investors.

PIMCO ultimately raised $4.18 billion for the BRAVO Fund III pitching it to institutional investors as a “private equity-style opportunistic fund with an expected emphasis on markets influenced by regulatory reform” including mortgage, real estate and personal loans.

The New Mexico State Investment Council which manages billions of dollars in revenue generated by leases and sales of public lands for the state of New Mexico ultimately invested $100 million in BRAVO III. The Pennsylvania Public School Employees’ Retirement System (PSERS) was another investor chipping in $250 million in 2017.

PIMCO launched the first in a series of “bank recapitalization and value opportunities” funds, BRAVO Fund I in 2011 raising $2.4 billion, according to a PSERS staff report to the retirement system’s board.

The $5.5 billion BRAVO Fund II which funded PIMCO’s investment in FGMC closed in 2013 with support from backers including the Teachers’ Retirement System of Oklahoma and the Nebraska Investment Council.

Last year PIMCO launched BRAVO Fund IV — a potential source of funding to keep FGMC above board. FGMC’s Chapter 11 bankruptcy filing is intended to give the company leeway to submit a plan of reorganization to keep its business alive and pay creditors over time.

A company affiliated with PIMCO, B2 FIE IV LLC, owns 100 percent of FGMC’s common stock. Another PIMCO-affiliated company, B2 FIE XI LLC, has agreed to provide “debtor-in-possession” financing to provide operational cash flow to FGMC, according to FGMC’s bankruptcy petition.

A spokesperson for PIMCO declined to comment on how its Bravo fund investments have performed or the future prospects of FGMC and non-QM mortgage lending.

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

{kind=link}