A stern warning from Federal Reserve Chair Jerome Powell that taming inflation “requires using our tools forcefully” even if that brings “some pain to households and businesses” sent stock prices tumbling Friday, but had surprisingly little impact on long-term interest rates.

Powell’s remarks at the annual Jackson Hole central banking conference in Wyoming raised the odds that the Fed will implement another 75 basis-point increase in the short-term federal funds rate at its next meeting, which concludes Sept. 21.

But the Fed doesn’t have such direct control over mortgages and long-term interest rates, which stayed put Friday as bond market investors stood firm on bets that the Fed will need to pivot next year and start cutting interest rates if the economy slows or enters a recession.

Yields on 10-year Treasury notes, which are useful indicators of which way mortgage rates are headed next, hovered around 3 percent after Powell’s address. Over the last 12 months, yields on 10-year Treasurys have climbed from a low of 1.26 percent to a 2022 peak of 3.48 percent on June 14.

Mortgage rates stabilize

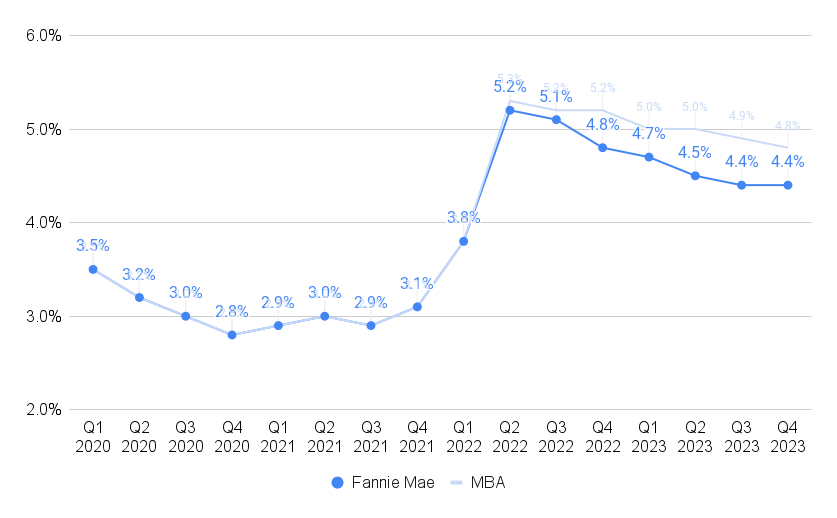

The Optimal Blue Mortgage Market Indices show rates for 30-year fixed-rate conforming loans also hit their 2022 peak of 6.06 percent on June 14. While long-term rates bounced back in August, mortgage industry groups think they’ve peaked and will ease next year.

Mortgage rates expected to ease

Source: Fannie Mae Housing Forecast, August 2022

In a forecast issued this week, Fannie Mae economists acknowledged the risk that the Fed will continue to be aggressive in raising short-term interest rates if inflation and job growth remain strong. But they anticipate less pressure on long-term interest rates including mortgages, due to expectations that a “modest recession” is looming next year and that the labor market will soften as the effects of tighter monetary policy take hold.

In a July forecast, economists at the Mortgage Bankers Association predicted a similar, but less pronounced pullback in mortgage rates.

But in his speech Friday, Powell seemed to be issuing a warning not to underestimate the Fed’s determination to bring down inflation.

“The Fed appears frustrated by market expectations — which we have never shared — of easing next year,” said Pantheon Macroeconomics Chief Economist Ian Shepherdson in a note to clients.

“The Fed can’t ease until inflation is clearly headed back to target, and wage growth has slowed markedly,” Shepherdson wrote. “The Chair’s message today is that the Fed thinks these conditions are unlikely to be met as soon as markets expect. We think he is probably right.”

Shepherdson said that while Powell acknowledged inflation has been driven by strong demand and tight supply constraints, “He left unsaid the point which we have been making for some time: Namely, that tight supply has facilitated a massive surge in margins, which likely will reverse, driving inflation down, now that inventories are returning to normal, or even above normal.”

Powell hinted that a 75 basis-point increase in the federal funds rate could be in the cards next month, although the decision will depend on the latest data. A third hike of that magnitude this year would bring the short-term benchmark to between 3 percent and 3.25 percent. In a June poll, members of the Federal Open Market Committee indicated that they envision raising the federal funds rate to just under 4 percent and keeping it there through the end of next year to tame inflation.

“July’s increase in the target range was the second 75 basis-point increase in as many meetings, and I said then that another unusually large increase could be appropriate at our next meeting,” Powell said. “We are now about halfway through the intermeeting period. Our decision at the September meeting will depend on the totality of the incoming data and the evolving outlook. At some point, as the stance of monetary policy tightens further, it likely will become appropriate to slow the pace of increases.”

The CME FedWatch Tool, which monitors futures contracts to calculate the probability of Fed rate hikes, shows traders on Friday were pricing in a 60 percent chance of a 75-basis point rate hike on Sept. 21.

While the Federal Reserve has direct control over the short-term federal funds rate, rates on long-term investments, such as Treasurys and mortgage-backed securities, depend largely on investor demand.

The Fed is one of those investors, however, having amassed more than $2.7 trillion in mortgage debt to help keep rates low during the pandemic and the “Great Recession” of 2007-09.

The Fed, which also holds $5.7 trillion in long-term Treasurys, has been trimming its $9 trillion balance sheet this summer. In June, the Fed began its “quantitative tightening” program by letting up to $17.5 billion maturing mortgage assets roll off its books each month.

Next month, the Fed is expected to increase the size of its mortgage roll-offs, to $35 billion a month. The pace of Treasurys rolloffs is expected to be even faster — $30 billion a month at first and increasing to $60 billion a month after three months.

The Fed’s $9 trillion balance sheet

Assets on the Federal Reserve’s balance sheet include $5.70 trillion in long-term Treasurys and $2.72 trillion in mortgage-backed securities. Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of St. Louis

While Powell did not provide additional insight on the pace at which the Fed intends to trim its balance sheet, he did allude to the Fed’s intention to use its “tools” — highlighting that short-term interest rates are not the only arrow in the central bank’s inflation-fighting quiver.

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance,” Powell said. “Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions.”

“While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses,” Powell said. “These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.”

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.

{kind=link}